Introduction: The Moral Alibi

I have never met anything other than sincere Muslims in my decades in Islamic finance. But this sincerity has proved to be irrelevant to Islamic finance.

After more than five decades of institutional development, billions in assets under management, and the establishment of global regulatory frameworks, Islamic finance has arrived at a profound and uncomfortable standstill. We have built an industry that looks like a bank, speaks like a bank, and creates debt like a bank, yet we continue to call it “Islamic.” When confronted with the empirical evidence of this failure—the persistent replication of Riba, the benchmarking against interest rates, and the avoidance of real-world risk—the industry unfailingly retreats into a singular, unassailable fortress: the “purity of intent.”

This is the moral alibi of our era. We operate under the comfortable shade of a collective excuse: that because our practitioners are sincere, because our scholars are pious, and because our community genuinely seeks a “Halal” alternative, the system must, by definition, be moving toward the truth. We treat sincerity (Niyyah) not as a private virtue for the afterlife, but as a structural variable that can somehow compensate for a broken architecture.

This is a delusion. Sincerity has been weaponised as a psychological buffer, a “Search Function” for comfort rather than truth. It allows the practitioner to live in the “Domain of Management” while pretending to remain in the “Domain of Obligation.” The hard truth is that sincerity is structurally irrelevant to systemic output. A sincere pilot cannot fly a plane whose wings are made of lead, and a sincere Muslim cannot operate a debt-logic architecture without producing Riba. We have traded the Command of Allah for the Comfort of Intent, and in doing so, we have built a graveyard of ethical aspirations.

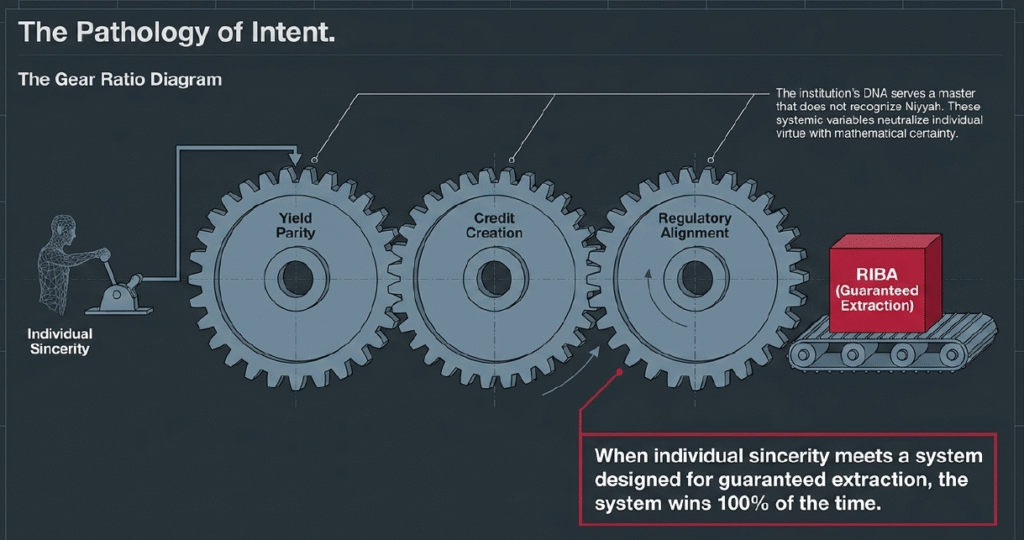

1. The Pathology of Intent

In the current sector, sincerity acts as a structural lubricant for compromise. Because the actor wants to do the right thing, they believe that a “just-compliant-enough” structure is a stepping stone rather than a permanent trap. We frame our failures as “temporary accommodations” or “stages of transition,” ignoring the fact that these stages have no end date.

This creates a fundamental rupture between the person and the institution. The individual may be deeply sincere, but the institution is mechanical and cold. The institution’s “DNA”—yield parity, credit creation, liquidity requirements, and regulatory alignment—serves a master that does not recognise Niyyah. These systemic variables neutralise individual virtue with mathematical certainty. Sincerity does not change the gear ratio of a Riba-machine; it only makes the operator feel better while they pull the lever. When individual sincerity meets a system designed for guaranteed extraction, the system wins 100% of the time. The tragedy is not that the people are bad; it is that their goodness is being used to stabilise a system that is structurally antithetical to their values.

2. The Scholar as a “Sanctifier of Substance”

The most visible casualty in this pathology is the traditional role of the scholar. We have moved from a historical tradition where scholars governed the movement of capital to one where they merely sanctify the intent of the transaction. In the contemporary model, the Shariah Board has been repositioned at the end of the deal-making process. They are asked to validate the language of a contract after the economic substance has already been fixed by conventional optimisation metrics.

The Fatwa has thus become a “Certificate of Sincerity.” It tells the customer: “You do not need to look at the mechanics of this debt-based instrument, because a Sincere Man has signed it.” This effectively kills the communal obligation of Hisbah (accountability) and replaces it with a procedural trust in a broken process. Certification signals that the moral question has been resolved, even when the underlying structure preserves the very risk asymmetry and extraction that the prohibition of Riba was meant to restrain. When review does not interrogate outcomes, compliance reduces to hollow performance. The issue is not the intention of the scholar; it is that their evaluative frame is now too narrow to address what the prohibition was actually designed to prevent.

3. The Illusion of the Banking Cage

We often blame the banking license for this failure. Critics and practitioners alike argue that the constraints of the fractional reserve system, the demands of central banks, and the necessity of capital adequacy force us into debt-logic. The narrative suggests that if we only had more regulatory freedom, the “Halal” nature of our finance would flourish. However, the data suggests a much darker reality.

Islamic banking assets comprise roughly 75% of the $5tn global industry. These are the assets under the strict “cage” of the banking license. 95% of these assets are debt, credit and lending assets benchmarked to interest. But look at the remaining 25%—dominated by Sukuk (20%). These operate in the capital markets, largely outside the strict fractional reserve constraints of traditional banking. Yet, they revert unerringly to debt and Riba.

Sukuk, marketed as “asset-backed certificates” or “participation certificates,” are consistently engineered to function as fixed-income debt. They prioritise principal protection, guaranteed return of capital through “purchase undertakings,” and benchmark-linked yields. Even with the freedom of the capital markets, the architects of Sukuk used that freedom not to innovate, but to imitate. This illustrates, to my great regret, the banking license is not the cause of the behaviour; it is merely a convenient outlet for it. The toxicity is not regulatory; it is foundational. It is a refusal to accept the reality of loss and the “Refusal to Collapse Time.”

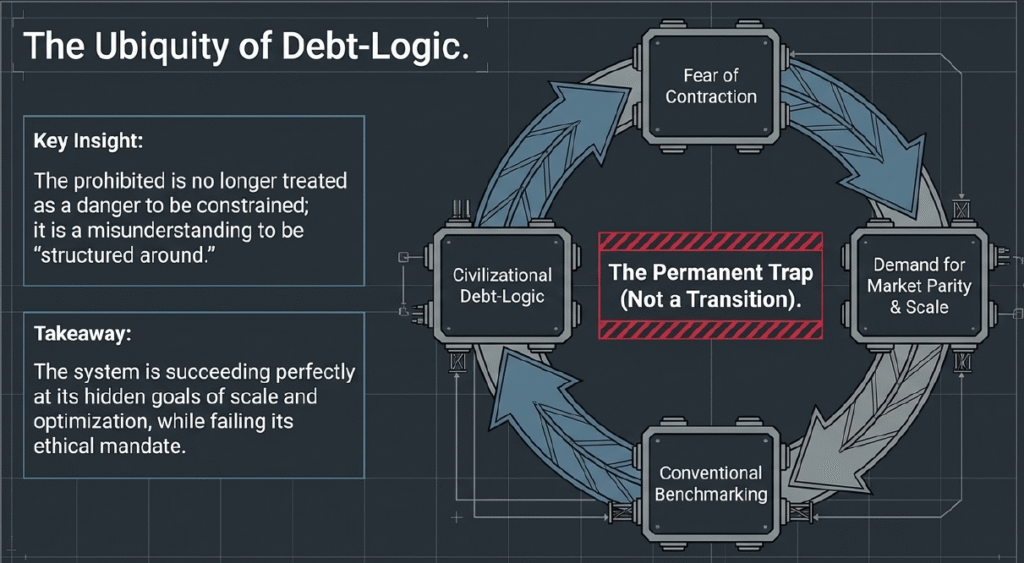

4. The Ubiquity of Debt-Logic

The problem is not the “Bank”; it is a civilizational Debt-Logic that has infected the modern Muslim mind. The industry has built many different pipes—Banks, SPVs, Takaful, Sukuk, and Fintech platforms—but they all carry the same contaminated water. This is because the “Optimisation” hierarchy governs every move.

When the goal is market parity, every instrument must mirror the conventional world. The investors demand the same returns, the risk committees demand the same certainty, and the institutional leadership shares the same “Fear of Contraction.” The $1tn Sukuk market proves that the “Death of Sincerity” is not an accident of law. It is a structural choice made by people who refuse to allow capital to be truly exposed to the uncertainty of the future. We have become the most reliable guardians of the mechanics we once declared war against. The prohibited is no longer treated as a danger to be constrained; it is treated as a misunderstanding to be “structured around.”

5. The Orthogonal Shift: From Heart to Spine

If sincerity is dead as a governing force, we must stop trying to “fix” the Muslims in the system and start fixing the system itself. We do not need better people in banking; we need a better Rail. We have spent fifty years waiting for a change of heart to lead to a change of structure, and it has not happened. There is no hint of it even beginning. It is time to accept that the “System Is the Outcome.”

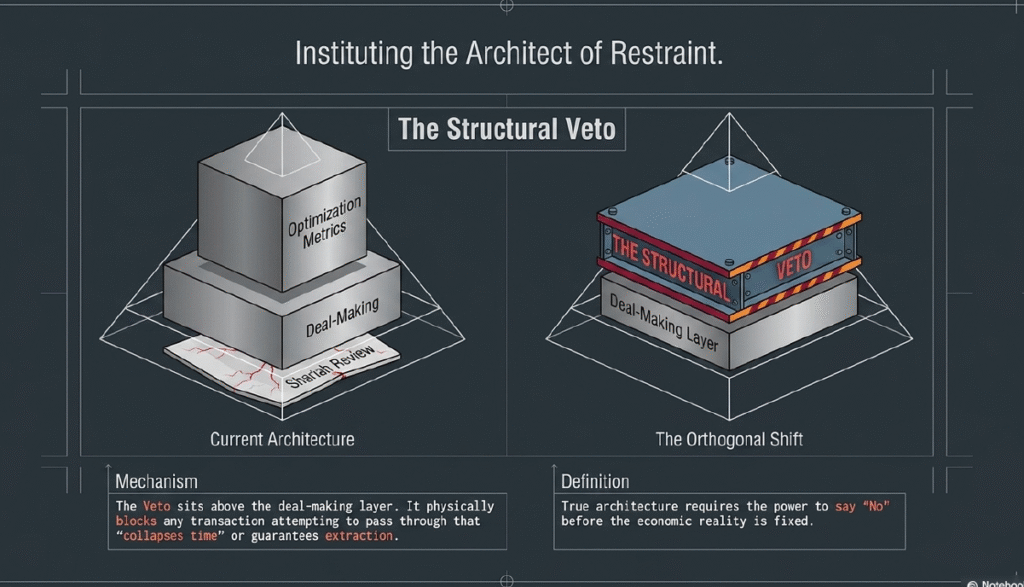

A true Islamic financial architecture must be so structurally sound that it produces Halal outcomes even if the operator is indifferent or even malevolent. We must move from a system that relies on “Sincere People” to a system that relies on Inviolable Mechanics—structures that are physically, legally, and mathematically incapable of creating Riba. This is the shift from the “Heart” to the “Spine.”

This requires the Structural Veto—the presence of an architect of restraint who sits above the deal-making layer and says “No” to any structure that collapses time or guarantees extraction. It requires the Asset-Backed Exchange (of assets that have not even been designed yet), where value is traded in reality rather than simulated in credit. It requires the Orthogonal Shift—the courage to operate outside the incumbent institutions and their eternal optimisation loops. We must stop trying to sanctify the bank and start building the Sovereign Rail.

Conclusion: The Baseline of Truth

Acknowledging the death of sincerity is not an act of cynicism; it is the ultimate act of honesty and the first step toward a genuine Exit. We must recognize that the industry is not failing despite its efforts; it is succeeding at its hidden goals of parity, scale, and optimisation. It has successfully preserved the substance of Riba while cleansing its form for a pious audience.

Submission does not require proof of competitive outperformance or the validation of a global benchmark. Its legitimacy derives from the Command of Allah swt, not from its ability to match the yield of a conventional competitor. Until we reverse the governing hierarchy—until obedience becomes sovereign and optimisation is correctly recognized as subordinate—we will remain structurally indistinguishable from the system we claim to critique.

The solution is the construction of a rail where the Veto sits above the deal, where time is not collapsed, and where Submission is the primary metric of success. We do not need a change of heart; we need an exit from dominant global debt and credit infrastructure. No other measure is appropriate for this endeavour of sincere Muslims. The rupture is complete, and the baseline of truth is the only place left to stand.