1. Purpose: From Diagnosis to Constraint Extraction

The preceding body of work (The Core Thesis) establishes a systemic conclusion: contemporary Islamic finance, despite significant institutional development and sincere intent, exhibits persistent convergence toward debt-equivalent outcomes.

This convergence is not treated here as a matter of isolated product design failure, nor as a function of individual institutional weakness. It is treated as a structural property of systems operating under stable incentive fields.

The purpose of this paper is therefore not to restate that diagnosis.

It is to extract from it a formal set of structural requirements that any alternative financial architecture must satisfy if it is to avoid reproducing the same equilibrium outcomes.

This represents a transition in focus:

- from explanation of system behaviour

- to derivation of necessary design constraints

2. Established Systemic Reality (Compressed Restatement)

Across the Core Thesis Series, a consistent set of dynamics has been identified:

- Financial systems reproduce equilibrium outcomes under persistent incentive structures

- Institutional survival pressures dominate declared design intent

- Product-level differentiation does not alter underlying system behaviour

- Compliance frameworks tend to stabilise replication rather than enable transformation

- Scale amplifies convergence rather than resolving it

From this perspective, convergence toward debt-equivalent structures is not an anomaly within Islamic finance. It is an expected outcome of the system’s structural environment.

This paper treats that conclusion as a starting condition.

3. Fundamental Constraint: Non-Reversion Requirement

Any alternative Islamic financial architecture must satisfy a primary structural requirement:

It must not revert to debt-equivalent equilibrium under scale, stress, or institutional optimisation pressure.

This implies that divergence cannot be treated as a matter of intention, ethical alignment, or governance preference.

Divergence must be structurally preserved.

If a system permits gradual reconstitution of conventional financial logic under alternative naming conventions, then it is not structurally distinct.

It is a reclassification layer operating on the same equilibrium substrate.

4. Constraint Placement: Architecture-Level Definition of Possibility

A central limitation of existing reform efforts is that constraints are applied primarily at the level of instruments and contracts.

However, system behaviour is not determined at the instrument level. It is determined at the level of structural possibility space.

Therefore:

constraints must operate at the level of system architecture, not financial product design

This implies a shift in design logic:

- from modifying financial instruments

- to defining which types of financial relationships can exist at all

In this framing, system design begins not with what is allowed, but with what is structurally excluded.

5. Invariance Under Scale

Scale is not a neutral expansion of system activity. It is a transformation pressure on structure.

Historical observation suggests that as systems scale, they tend to:

- standardise financial relationships

- increase liquidity dependence

- optimise for regulatory compatibility

- converge toward dominant market forms

Therefore, any alternative architecture must ensure:

its governing constraints remain invariant under scale expansion

If scale introduces gradual relaxation of structural distinctions, convergence will re-emerge through optimisation behaviour rather than explicit design failure.

6. Institutional Incentive Neutralisation

Institutions are not neutral actors. They are incentive-processing systems optimised for:

- continuity

- survivability

- capital access

- efficiency under constraint

In most financial systems, these incentives naturally align with convergence toward dominant equilibrium structures.

Therefore, a replacement architecture must ensure that:

institutional optimisation does not imply structural convergence

This requires a separation between institutional survival logic and system-level design integrity.

Without this separation, institutions will systematically drift toward the most stable and replicable financial forms available within their environment.

7. Decoupling from External System Determinants

Existing financial systems are deeply integrated with external structures including:

- liquidity infrastructure

- benchmark formation systems

- regulatory frameworks

- settlement and clearing systems

- capital pricing mechanisms

These external systems are not neutral. They encode assumptions about how financial systems should behave.

Therefore:

structural dependence on external financial infrastructure imports behavioural convergence pressures

An alternative architecture must therefore reduce dependency on external system logic, or ensure that such dependencies do not determine internal structure.

8. Stress Condition Integrity

System behaviour under normal conditions is not sufficient to validate structural integrity.

The critical test is behaviour under stress conditions, including:

- liquidity contraction

- capital scarcity

- competitive pressure

- institutional survival stress

Under such conditions, systems tend to revert to dominant equilibrium forms unless constraints are structurally robust.

Therefore:

system constraints must remain stable under stress without identity drift or functional reversion

If stress alters system behaviour toward conventional financial replication, structural distinction is not preserved.

9. Category-Level Constraint Requirement

One of the key findings of the Core Thesis Series is that equilibrium systems are preserved not only through instruments, but through financial categories themselves.

Therefore:

effective constraint must operate at the level of category definition, not instrument modification

Partial restriction within existing categories is insufficient, as it allows structural recombination into equivalent outcomes.

Only category-level restructuring or elimination can prevent systemic reconstruction of the same equilibrium under new forms.

10. Non-Replicability as a Validity Condition

A structurally distinct financial architecture must satisfy a strict condition:

it must not be reducible back into conventional financial templates through reinterpretation or decomposition

If a system can be mapped back into familiar debt-based or benchmark-based structures, then convergence has not been eliminated; it has been reformulated.

Therefore, non-replicability becomes a necessary condition of validity.

This does not imply opacity or complexity. It implies structural irreversibility of form.

11. Consolidated Structural Requirement Set

From the analysis above, the following necessary conditions emerge for any non-convergent Islamic financial architecture:

- Structural divergence must be preserved under scale and stress

- Constraints must operate at the level of system architecture, not instruments

- Institutional incentives must not imply convergence under optimisation

- External financial systems must not define internal structural behaviour

- Dependency on conventional infrastructure must not determine system outcomes

- Category-level financial structures must be redefined or eliminated where necessary

- System identity must remain invariant under stress conditions

- The architecture must be non-replicable into prior equilibrium forms

These are not preferences. They are structural requirements implied by observed system behaviour.

12. Transition: From Constraints to System Outcomes

The requirements defined in this paper specify what a viable alternative architecture must avoid and preserve structurally.

However, constraints alone do not define a functioning system.

The next stage of analysis must therefore address a further question:

What outcomes must such an architecture necessarily produce in real economic activity?

This includes the behaviour of capital flows, risk distribution, liquidity formation, and the relationship between financial structure and productive economic activity.

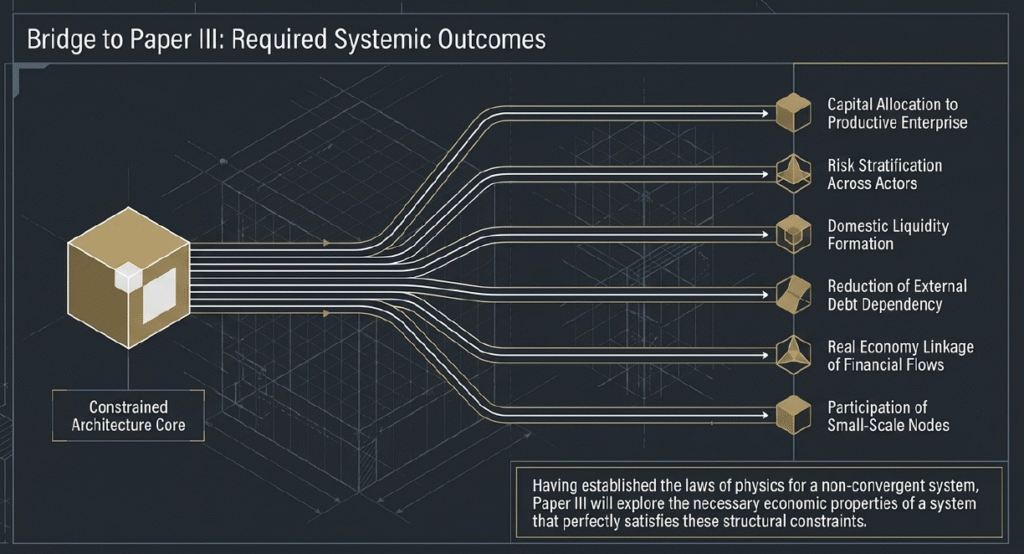

13. Bridge to Paper 3: Required Economic Outcomes of the System

Having defined structural constraints, the next step is to define the necessary properties of a system that satisfies them.

This includes:

- capital allocation to productive enterprise

- risk stratification across economic actors

- domestic liquidity formation

- reduction of external debt dependency

- real economy linkage of financial flows

- stability mechanisms and reserve logic

- participation of small-scale economic nodes within system architecture

Paper 3 will therefore move from:

structural constraints

to

required systemic outcomes

Closing Note

This paper completes the transition from systemic diagnosis to formal constraint extraction.

The architecture that follows cannot be meaningfully understood without first recognising the necessity of these structural conditions.