Paper III

Required Economic Outcomes of a Constraint-Based Financial Architecture

(From Structural Requirements to System Behaviour)

1. Purpose of This Paper: From Constraints to Outcomes

Paper II defined the structural requirements of a non-convergent financial architecture. Its focus was on boundaries: what the system must not replicate, where invariance must hold, and the structural conditions required to prevent convergence into conventional debt-based financial systems.

Those constraints establish structural integrity. Structural integrity alone, however, is insufficient. A viable financial architecture cannot be defined only by what it avoids. It must also generate coherent economic outcomes in the real economy. Constraint without productive consequence remains theoretical containment. Structural discipline without functional output remains economically incomplete.

This paper therefore shifts from structural requirement to economic requirement. Its focus is not what the architecture must resist, but what it must consistently produce under real operating conditions.

2. From Structural Integrity to Functional Design

Structural validity and functional legitimacy are separate requirements.

A system may preserve internal discipline while remaining economically inactive. Equally, a system may generate activity while reproducing the same financial dependencies it was intended to avoid. Neither condition alone is sufficient.

A viable architecture must preserve structural non-convergence while also generating recurring economic function. These two requirements must coexist. Structural integrity prevents drift into replication. Functional legitimacy ensures the architecture remains economically relevant. Together they define the minimum conditions for viability.

3. Core Requirement: Productive Capital Flow

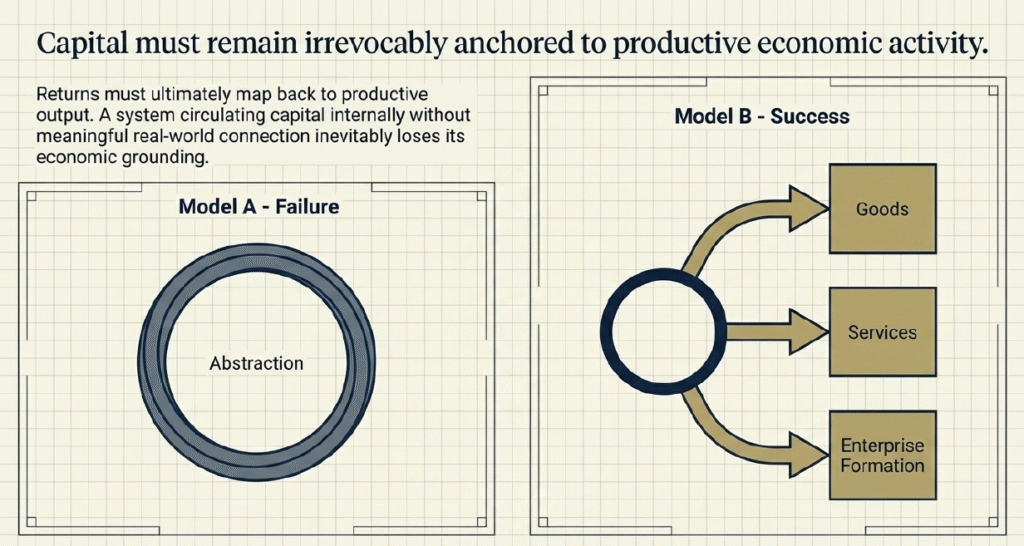

Capital must remain anchored to productive economic activity. Its movement must connect directly to the production of goods, services, enterprise formation, and recurring commercial continuity.

A financial system that circulates capital internally without meaningful productive output becomes increasingly abstract over time. Capital may move, positions may update, and balances may appear active, but if the system fails to connect with productive reality it loses economic grounding.

Returns must ultimately map back to productive output. This remains the central requirement. The architecture must operate as a mechanism for directing capital into productive environments rather than reinforcing abstraction detached from economic production.

4. Risk Stratification as Structural Necessity

Capital enters any system with materially different requirements. Some participants prioritise stability. Others require flexibility. Others accept greater volatility in exchange for frontier exposure and higher variance.

These differences are structural and cannot be collapsed into uniform capital treatment without weakening participation and distorting allocation.

A viable architecture must preserve differentiated risk exposure across layers. Stability-seeking capital must remain structurally protected. Moderate-risk capital must retain productive flexibility. Higher-variance capital must remain able to participate in more dynamic allocation without destabilising conservative capital.

Risk therefore remains present. The system does not eliminate it. The requirement is structured organisation rather than forced homogenisation.

5. Domestic Capital Circulation and Economic Anchoring

Capital must circulate meaningfully through productive domestic systems.

This is not a requirement of economic isolation. It is a requirement of continuity. Where productive capital repeatedly circulates through enterprise, labour, local services, and recurring trade, resilience strengthens over time. Economic continuity becomes less dependent on external debt channels and more closely tied to internally productive activity.

Financial architecture therefore functions as a reinforcing layer around productive capacity. It strengthens circulation within the economic environment that sustains it.

6. Stability Without Debt Dependency

Conventional financial systems frequently generate stability through leverage, refinancing cycles, and debt expansion.

A constraint-based architecture requires a different source of stability. Stability must emerge through productive output, diversified allocation, reserve discipline, and continuity across multiple productive environments.

This is a structural distinction. Debt-based stability often expands through future obligation. Constraint-based stability emerges through productive continuity and disciplined capital placement.

Stability remains essential. The source of that stability changes.

7. Distributed Economic Participation

A viable architecture must remain accessible across economic scales. Participation cannot be structurally limited to institutions or large capital allocators.

The system must support productive activity across micro-enterprises, small and medium businesses, household capital, and institutional capital simultaneously. Low-friction investor access forms part of this requirement. Participation thresholds must remain sufficiently open to allow meaningful contribution across a broad range of capital sizes.

This matters because resilience strengthens when productive participation is distributed. Economic concentration narrows resilience. Broad participation widens it and creates stronger continuity across the system.

8. Liquidity Function Without Debt Structures

Every financial architecture requires liquidity. Capital must hold position, transition between allocations, remain available, and move when required.

Conventional systems often achieve this through debt-linked instruments and interest-bearing structures. A non-convergent architecture still requires equivalent liquidity function without replicating those forms.

Liquidity therefore remains a functional necessity independent of traditional debt structures. The architecture must preserve movement and availability while maintaining structural non-replication.

Liquidity remains necessary. Only the structure through which it exists changes.

9. The Fruit Seller Principle

(Baseline Economic Continuity Node)

Certain productive activity persists under nearly all conditions. Essential local trade, food distribution, and recurring necessity-based services continue through expansion and contraction alike.

Their importance is not defined by scale. It is defined by continuity.

A fruit seller operating through changing economic conditions represents a persistent productive node. Activity of this kind forms the continuity layer of the broader economy. These nodes remain economically relevant even when more volatile sectors contract.

Structural resilience begins with continuity in necessary productive activity. These baseline nodes anchor circulation and reinforce stability through persistence.

10. System-Wide Stability Through Aggregation of Productive Nodes

Individual productive nodes do not move uniformly. Some expand while others contract. Some remain stable across changing conditions.

Across a distributed architecture this variation creates balance. Productive diversity disperses concentration and reduces volatility clustering. Stability emerges through aggregation rather than through reliance on increasingly abstract financial layering.

Macro continuity therefore becomes the cumulative effect of distributed productive participation across multiple environments and activity types.

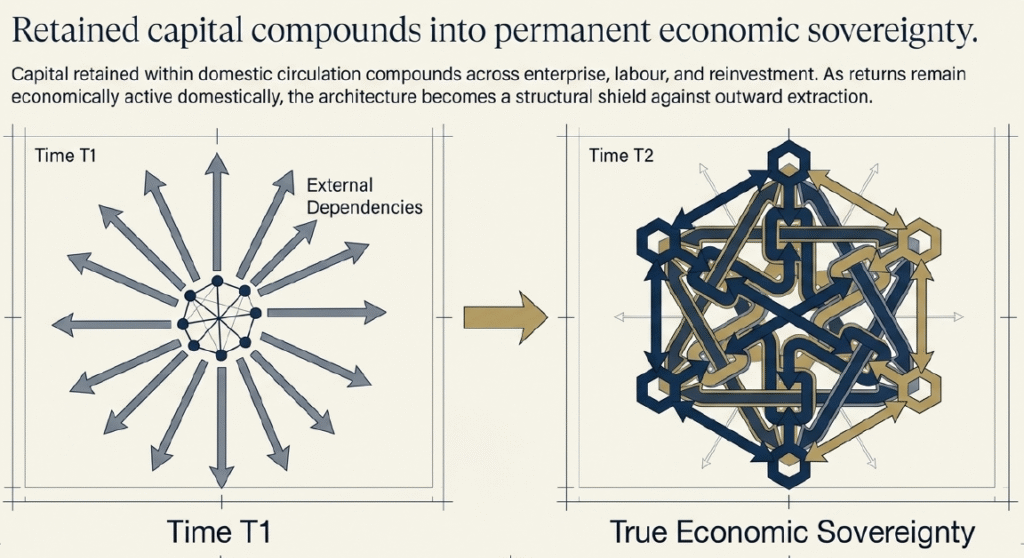

11. Sovereignty and Internal Capital Strengthening

A viable architecture must strengthen internal productive capacity over time.

Capital retained within productive circulation compounds across enterprise formation, labour participation, local services, and reinvestment. Returns remain economically active within the domestic environment and reinforce recurring productive activity.

Over time this reduces external dependency and strengthens economic sovereignty. The financial architecture becomes a reinforcing structural layer within domestic productive systems rather than a mechanism of outward extraction.

12. Functional Summary: What the System Must Achieve

A viable non-convergent financial architecture must allocate capital into productive economic activity, preserve differentiated risk exposure, maintain broad participation across capital sizes, keep investor access structurally open, preserve liquidity without debt replication, strengthen domestic productive circulation, remain resilient through persistent productive activity, generate stability through productive aggregation, support both micro and institutional productive nodes, and reinforce internal economic sovereignty over time.

Together these outcomes define the minimum economic behaviour required of the system.

13. Transition to Paper IV

Paper II defined structural constraints. Paper III defines the economic outcomes required within those constraints.

The next stage moves from required outcomes toward available structural components.

Paper IV – The Available Building Blocks of a New Financial Architecture introduces the practical building blocks from which the architecture can be assembled. Having defined both structural boundaries and required economic behaviour, the next paper identifies the available mechanisms, components, and system primitives capable of supporting a viable non-convergent financial architecture.

Closing

This paper defines the required economic behaviour of a viable alternative financial architecture.

The next stage moves from required outcomes toward the available building blocks from which the architecture itself can be constructed.