Gravity, Selection and Emergent Economic Outcomes

1. Introduction: Systems, Constraint, and Emergent Structure

Economic and financial outcomes in Muslim contexts are often explained through reference to prohibition, compliance, or institutional reform. These explanations typically assume that constraint operates as a fixed rule applied uniformly across a neutral environment. This paper proposes a different framing.

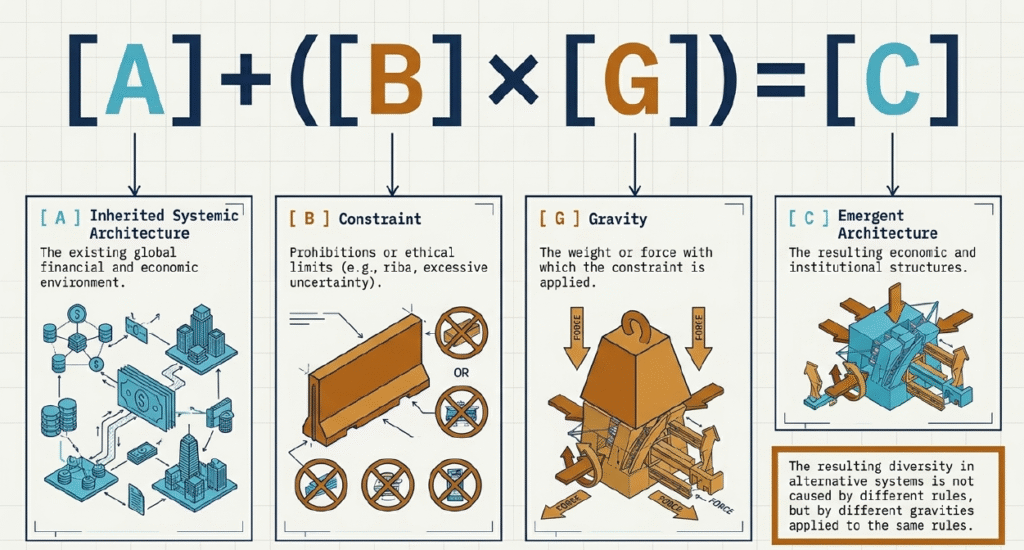

The analysis begins with the existing systemic architecture (A): the global financial and economic environment in which all actors operate. This architecture is not defined by religion or ethics, but by accumulated institutional structures, market conventions, legal frameworks, and capital market infrastructure. It is historically shaped around debt-based finance, risk pricing mechanisms, and deeply embedded liquidity systems.

Within this inherited field, Muslim actors and institutions introduce constraint (B), including prohibitions such as riba and other limits on financial behaviour. However, the presence of constraint alone does not determine outcomes.

The central variable is the weight or gravity applied to constraint (G). Different levels of gravity produce different patterns of selection from A, different forms of adaptation, and ultimately different emergent architectures (C). The purpose of this paper is to formalise this relationship between inherited structure, constraint, and emergent outcome.

2. Existing Systemic Architecture (A): The Inherited Field

The existing systemic architecture (A) is best understood as a layered aggregation of institutional and economic components. It includes global banking systems, capital markets, corporate financing structures, legal frameworks governing contracts and ownership, payment infrastructure, and established investor behaviour.

Crucially, A is not neutral. It is historically optimised around specific forms of capital formation, particularly debt-based expansion, maturity transformation, and leverage-driven liquidity creation. These structures are embedded not only in institutions, but in expectations, pricing models, and regulatory regimes.

A also contains multiple alternative components—equity structures, trade mechanisms, partnership models, and asset-based transactions—but these are not dominant in the global configuration. They exist within the system, but are not the primary organising logic.

This distinction is important. The inherited field already contains a wide set of possible financial mechanisms. The question is not whether these mechanisms exist, but which of them are selected, excluded, or prioritised when constraint is applied.

3. Constraint (B) and the Concept of Weighting

Constraint (B) refers to prohibitions or limits applied within Muslim systems, most notably the prohibition of riba, but also extending to related principles such as excessive uncertainty or unjust enrichment. However, constraint should not be understood as binary.

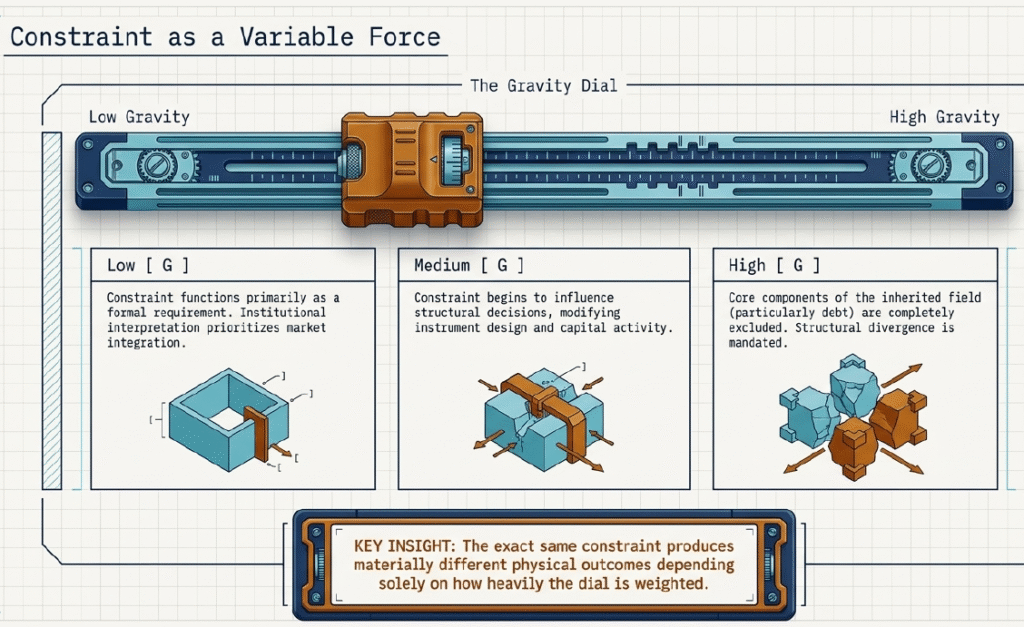

In practice, constraint is applied with varying degrees of gravity or weight (G). This weighting determines how strongly the constraint influences decision-making at both institutional and behavioural levels.

At low weighting, constraint functions primarily as a formal requirement. At higher weighting, it begins to influence structural decisions, including what types of financial instruments are admissible and which forms of capital activity are excluded entirely.

Weighting operates at multiple levels:

- institutional interpretation and enforcement

- market structuring practices

- individual participation decisions

The key insight is that the same constraint can produce materially different outcomes depending on how strongly it is applied. Constraint does not operate in isolation; it interacts with the inherited systemic architecture (A), filtering and reshaping it according to its applied gravity.

4. Selection from A: The First Point of Divergence

The first structural effect of constraint is not adaptation but selection from the existing systemic architecture (A). Once constraint is introduced, the system must determine which elements of A remain admissible, which require modification, and which are excluded.

At low levels of constraint weighting, large portions of A remain fully accessible. Debt-based structures, including conventional lending and interest-bearing instruments, remain within the effective field of admissibility, even if modified at the margins.

At higher levels of weighting, selection becomes narrower. Certain core components of A—particularly debt-linked mechanisms—are excluded from the admissible set. This fundamentally changes the space within which financial structures can be constructed.

This selection process is critical because it occurs before any new structure is formed. The shape of the outcome is therefore determined not only by how systems adapt, but by what they are allowed to carry forward from the inherited field in the first place.

The decision to replicate, modify, or exclude debt-based structures is itself an expression of constraint weighting, not a neutral continuation of inherited architecture.

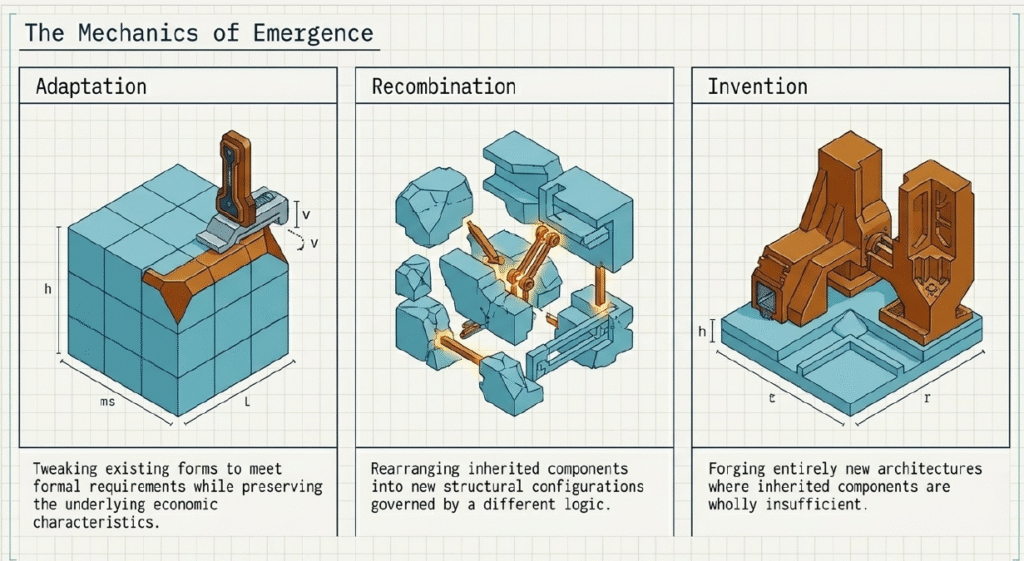

5. Emergent Outcomes (C): Adaptation, Recombination, and Invention

Once selection from A has occurred under a given constraint weighting, the system produces emergent outcomes (C). These outcomes typically fall into three categories: adaptation, recombination, and invention.

Adaptation occurs when existing structures are retained and modified to fit within constraint boundaries. In finance, this is often seen in structures that replicate economic characteristics of debt while modifying contractual form.

Recombination occurs when multiple components of A are rearranged into new configurations. This may involve combining trade mechanisms, ownership structures, and intermediary vehicles to produce financial flows that differ structurally from their conventional counterparts.

Invention occurs when the inherited system is insufficient to meet the demands imposed by constraint. In such cases, new architectures emerge through novel combinations or extensions of existing components. Importantly, “new” does not necessarily mean ex nihilo creation. It often refers to previously available elements of A being selected and combined under a different governing logic.

The type of outcome produced depends directly on the weight applied to constraint. Low weighting tends toward adaptation, medium weighting toward recombination, and high weighting increases the probability of invention or structural divergence.

6. Islamic Finance as Constraint-Weighted Selection

Modern Islamic finance provides a clear illustration of constraint-weighted selection within an existing systemic architecture. The inherited field (A) consists primarily of global debt-based financial systems, alongside alternative mechanisms such as equity, trade finance, and asset-based transactions.

The introduction of riba prohibition (B) requires selection from this field. However, the observed outcome in many markets reflects relatively low to medium constraint weighting at the selection stage. As a result, debt-like economic functions are often retained through modified contractual structures.

In practice, this leads to architectures that closely resemble conventional finance in economic substance, while differing in formal structure. Instruments such as murabaha-based financing and certain sukuk structures often preserve cash-flow characteristics similar to debt, even while being structured through asset or trade mechanisms.

This does not imply failure of constraint, but rather indicates a specific weighting of constraint within the selection process. The result is a hybrid architecture: partially distinct in form, but closely related to the underlying inherited system.

Different weighting would produce different selection outcomes, and therefore different financial architectures.

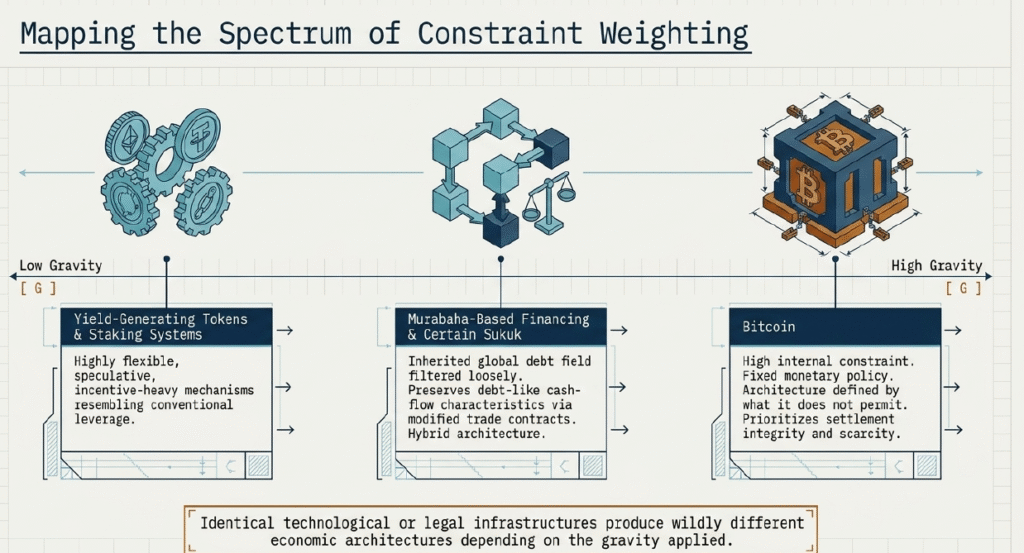

7. Crypto as a Spectrum of Constraint Weighting

Cryptocurrency markets provide a useful contemporary example of constraint weighting within a relatively open and evolving systemic architecture.

At one end of the spectrum, Bitcoin represents a system with high internal constraint weighting. Its monetary policy is fixed, its structural flexibility is limited, and its design prioritises settlement integrity, scarcity, and ownership over functional expansion. The architecture is defined by what it does not permit, including discretionary issuance and complex internal financial engineering.

At the opposite end are highly flexible and speculative token systems characterised by rapid issuance, incentive-heavy mechanisms, and structures resembling leveraged or yield-generating instruments. These systems apply relatively low internal constraint, allowing broad experimentation but also greater instability and fragility.

Within this field, Muslim participation reflects a second layer of constraint application. High constraint weighting tends to favour Bitcoin-like structures based on ownership and settlement. Lower weighting permits participation in yield-generating mechanisms, staking systems, and other forms of financial engineering that resemble conventional return structures.

The key observation is that identical technological infrastructure produces different economic architectures depending on the weight applied to constraint at both system and participant levels.

8. Extension: Other Sectors (Alcohol and Gambling)

The same structural logic applies beyond finance. In sectors such as alcohol and gambling, inherited systemic architecture (A) includes established consumer markets, distribution systems, and entertainment industries.

When constraint (B) is introduced, outcomes again depend on weighting (G). At low weighting, these sectors may remain partially integrated through regulation or limitation. At higher weighting, they are excluded from the admissible economic field, requiring substitution through alternative forms of consumption, entertainment, or social infrastructure.

These substitutions may include the development of alternative hospitality environments, leisure activities, or non-extractive entertainment systems. The resulting architecture differs depending on how strongly constraint is applied.

9. Conclusion: Constraint Weighting as an Architectural Variable

This paper has proposed a structural framework for understanding Muslim economic outcomes through the interaction of three elements: the existing systemic architecture (A), constraint (B), and the weight applied to constraint (G). The interaction of these elements produces emergent economic and institutional architectures (C).

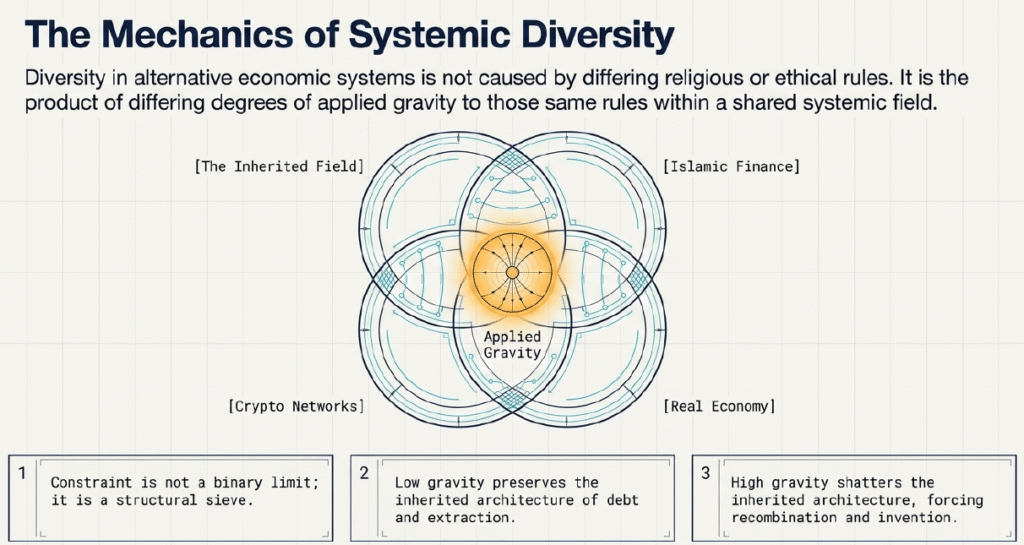

The central argument is that constraint does not operate as a binary switch. Instead, it functions as a variable force whose weight determines how systems select from inherited structures, how they exclude certain components, and how they recombine or generate new forms of organisation.

Low constraint weighting tends to preserve existing architecture with limited modification. Medium weighting produces hybrid structures combining inherited and adapted components. High weighting increases the likelihood of recombination or entirely new architectural formation where inherited systems are insufficient.

The resulting economic diversity across Muslim contexts is therefore not solely the product of differing prohibitions, but of differing degrees of applied gravity to those same constraints within a shared inherited systemic field.

Contribution to Core Thesis

This paper contributes directly to my Core Thesis: that constraint generates Alpha. It extends this principle by demonstrating that constraint is not simply a limiting factor, but an architectural variable. The alpha-generating properties of constraint depend on how strongly it is weighted, and how it reshapes selection, recombination, and invention within existing systemic structures.