The Rational Convergence of Muslim Consumers Toward Debt

1. Purpose of This Analysis

Debt adoption in retail Islamic finance is often explained through weak scholarship, poor execution, or insufficient innovation in product design. These explanations misread the phenomenon. They focus on surface-level implementation while ignoring structural incentives that govern consumer behaviour.

This paper examines a different proposition. Retail debt convergence is not a deviation from expected outcomes. It is a rational equilibrium produced when consumers operate within financial systems that make debt both accessible and functionally efficient, and where the effective weight of religious constraint is dynamically reweighted through institutional validation mechanisms.

The analysis is descriptive. It does not evaluate intent, moral positioning, or religious correctness. It focuses on structural behaviour under incentive and constraint architecture.

2. The Retail Financial Environment

Retail financial decision-making occurs within a constrained environment defined by income timing, liquidity needs, and consumption pressure. Consumers must continuously allocate resources across essential categories such as housing, transport, healthcare, and consumption smoothing. Within this environment, debt is not an external financial instrument. It is embedded into the structure of modern financial systems.

Credit is widely accessible. Repayment structures are standardised. Integration with income flows is routine. In most cases, debt represents the default mechanism for resolving liquidity mismatches.

As a result, consumer behaviour is shaped by constrained choice sets rather than abstract financial idealisation. Decisions are made within system-defined boundaries.

3. Debt as a Rational Consumption Mechanism

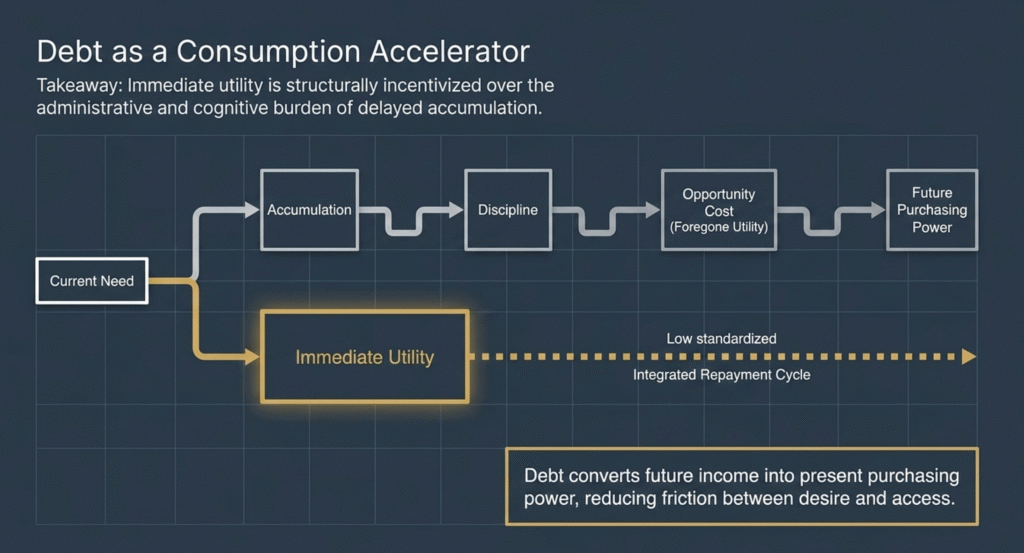

At the retail level, debt functions primarily as a mechanism for accelerating consumption. It converts future income into present purchasing power. It reduces friction between desire and access. It resolves the timing mismatch between income and expenditure.

From a consumer perspective, the incentives are clear. Immediate consumption produces immediate utility. Delayed consumption requires accumulation, discipline, and opportunity cost in the form of foregone present utility. Debt removes these constraints. Repayment structures are predictable and integrated into income cycles, reducing cognitive and administrative burden.

Within this framework, debt is not irrational behaviour. It is an efficient allocation mechanism under conditions of liquidity constraint. Rational behaviour therefore converges toward debt when alternative constraints are not strongly binding.

4. Religious Constraint and Its Effective Reweighting

Within Muslim consumer populations, an additional constraint exists in the form of riba prohibition. However, this constraint does not operate as a fixed binary restriction in practice. Its effective weight in decision-making is dynamically shaped by institutional structures.

Where prohibition is interpreted through fatwa-backed financial products that replicate debt-like functionality, the constraint is not removed — it is reclassified. This produces a structural shift: the consumer is no longer evaluating a direct prohibition but a permitted financial instrument that maps onto prohibited economic form with institutional validation.

As a result, the constraint becomes reweighted rather than absolute. Behaviour is therefore determined not only by incentive strength, but by the interpreted status of the constraint at the point of decision. Where incentives are strong and constraint weight is reduced through validation, convergence toward debt remains the rational outcome.

5. Islamic Retail Financial Products and Functional Substitution

Islamic retail finance emerges within this environment as a mechanism of functional substitution. At a structural level, many Islamic financial products reproduce the economic outcomes of conventional debt while modifying contractual or legal form.

This allows two conditions to be met simultaneously: access to consumption financing and reduction of perceived religious friction. The result is not divergence from conventional financial behaviour but alignment of product structure with demand under a reweighted constraint environment.

The underlying incentive structure remains unchanged. However, the perceived binding strength of constraint is modified through institutional classification. As a result, convergence occurs at the level of function, even where form differs.

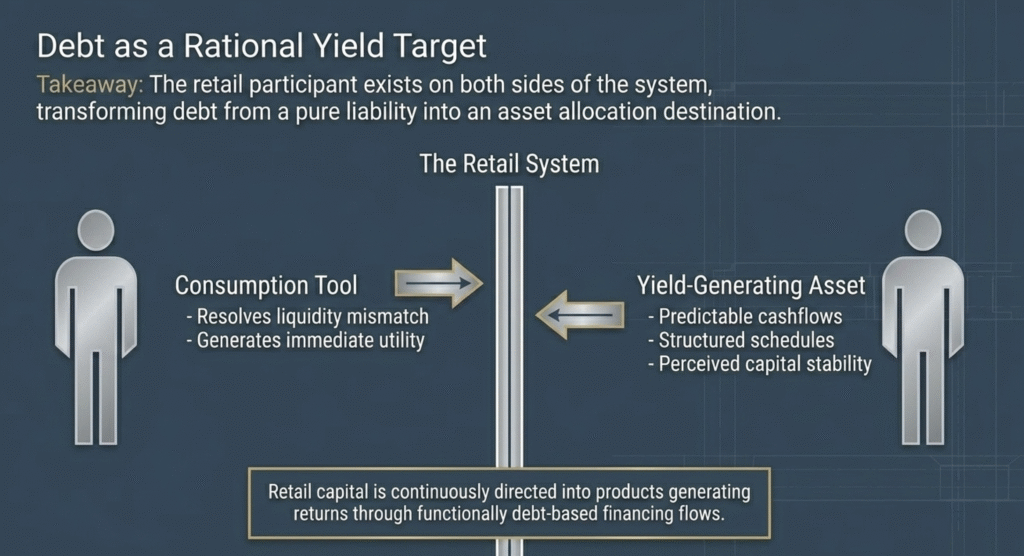

6. Debt as a Rational Yield Target

Once debt-based structures become normalised in consumption, a secondary shift occurs at the level of capital allocation. Debt instruments transition from consumption tools into yield-generating assets.

For retail participants, these instruments offer: predictable cashflows, structured repayment schedules, perceived capital stability, and accessible entry points. This creates a rational pathway for capital allocation into debt-linked structures. Within Islamic retail finance, this dynamic becomes particularly pronounced. Retail capital is increasingly directed into products that generate returns through exposure to financing flows that are functionally debt-based, even where they are structurally reclassified.

The consumer therefore participates in the same system from both sides: as borrower in consumption and as investor seeking yield. Debt becomes simultaneously a liability mechanism and an asset allocation destination.

7. Secondary Effects on Interpretation and Conviction

Retail convergence produces secondary effects beyond financial behaviour. In some cases, repeated engagement with structurally similar products creates interpretive ambiguity. Functional similarity between conventional and Islamic financial products can blur distinctions between form and substance in applied economic contexts. This leads to uncertainty in how religious constraints are interpreted in practice.

In other cases, the opposite effect occurs. Where products successfully resolve both consumption needs and perceived compliance concerns, they reinforce conviction in their legitimacy. The alignment of utility and institutional validation strengthens consumer confidence in the system.

The outcome is not uniform across individuals. However, in both cases, financial structure begins to shape interpretive frameworks through repeated exposure to system outcomes. Religious interpretation becomes partially mediated by financial experience.

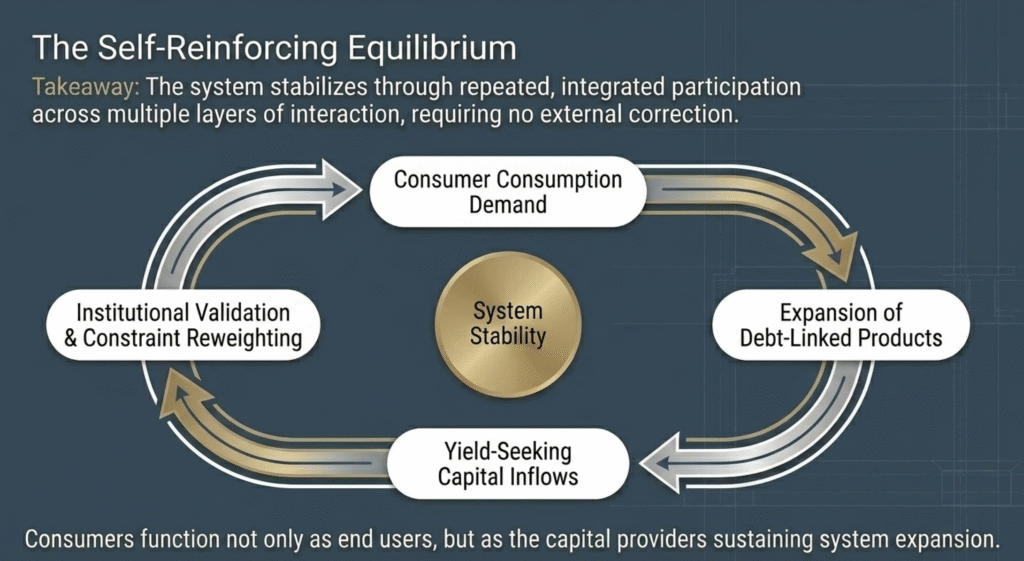

8. Feedback Loop: Retail Convergence and System Reinforcement

The interaction between consumption demand, product design, capital allocation, and constraint reweighting produces a reinforcing feedback loop.

Consumer demand drives the expansion of debt-linked financial products. These products attract both borrowers and yield-seeking participants. Capital inflows reinforce product scale and system stability. Institutional validation mechanisms simultaneously reduce effective constraint weight, further strengthening participation rates.

This creates a self-reinforcing equilibrium. Consumers function not only as end users of financial products but also as participants in sustaining their expansion through capital allocation. The system stabilises through repeated participation rather than external correction. Debt convergence is therefore reinforced across multiple layers of interaction.

9. Functional Summary

At the retail level, debt emerges as a rational consumption mechanism under standard incentive conditions. Where constraints such as religious prohibition are not uniformly binding, and where institutional validation mechanisms reweight the perceived status of those constraints, convergence toward debt-based structures is the expected outcome.

Islamic retail financial products operate as functional substitutes that preserve utility while reclassifying constraint status. However, they do not alter the underlying incentive environment that produces convergence. Debt-linked instruments further evolve into yield-generating assets at the retail capital level, embedding them within both consumption and investment behaviour.

The result is a system in which debt operates simultaneously as: a consumption mechanism, a structurally adapted financial product, a capital allocation instrument, and a reclassified constraint environment. This configuration produces a stable equilibrium driven by incentives and constraint interpretation rather than intent.

Closing Observation

Retail debt convergence is not an anomaly requiring behavioural correction.

It is a predictable outcome of rational decision-making within an environment where debt is structururally efficient, widely accessible, and where the effective weight of constraint is mediated through institutional validation structures that reclassify debt-like instruments as permissible.